In the article The November increase in the NBP reference rate affects the maximum interest rate in transactions between related parties, we wrote that in the environment of interest rate increases, when determining the interest rate on loans concluded between related parties, one should always verify whether the interest rate specified in the loan agreement is market-based at the time of concluding the financial transaction. Therefore pay attention to whether all the terms of the transaction are market-based and whether the interest rate of the transaction does not exceed the maximum interest rate

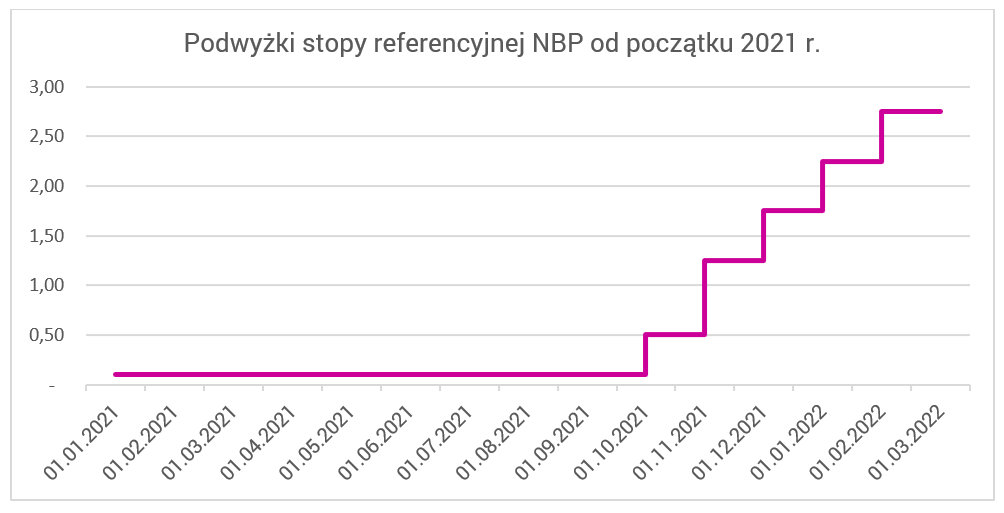

As of November 2021, the trend of interest rate changes by the NBP Monetary Policy Council remains unchanged. Both in December 2021 and January, February 2022. MPC decided to raise interest rates – currently the reference rate is 2.75% per annum.

Some economists indicate that the NBP’s reference rate may eventually be raised even to 4.25% p.a. still in 2022. Such a rapid change in interest rates, which has already taken place over several months (from 0.10% at the beginning of October 2021 to 2.75% in February 2022), significantly affects interest rates on loans, borrowings and bonds in the Polish zloty.

Each increase of the NBP reference rate changes the maximum allowed interest rate specified in Article 359 of the Civil Code.

Changes in the maximum interest rate in recent years are shown in the table below.

| Effective from: | Stopa referencyjna NBP (% w skali rocznej) | Maximum interest rate (% on an annual basis) |

| 05.03.2015 | 1.50 | 10.00 |

| 18.03.2020 | 1.00 | 9.00 |

| 09.04.2020 | 0.50 | 8.00 |

| 29.05.2020 | 0.10 | 7.20 |

| 07.10.2021 | 0.50 | 8.00 |

| 04.11.2021 | 1.25 | 9.50 |

| 09.12.2021 | 1.75 | 10.50 |

| 05.01.2022 | 2.25 | 11.50 |

| 09.02.2022 | 2.75 | 12.50 |

The increase also changes the level of the interest rate on the financing for which the parties to the financing transaction would have entered into the financing transaction. As a consequence, related parties in a financial transaction have to ensure that the arrangements of the agreement concerned continue to represent market conditions on which unrelated parties would also enter into the transaction.

What steps can be taken to avoid being challenged on the terms of financial transactions?

In the case of contracts concluded in the past

If you prepare a benchmarking analysis for a financial transaction, you should check whether it is up to date. Under the CIT Act, such a benchmarking analysis must be updated at least every three years, unless a change in the economic environment significantly affects the analysis prepared justifies updating the benchmarking analysis.

In the case of contracts with variable interest rates and where the benchmarking analysis has not been updated within the last three years or the current interest rate on the transaction is not within the range shown in the analysis, we recommend updating the benchmarking analysis based on the latest market data.

In the case of fixed-rate contracts, where the benchmarking has not been updated in the last three years, we also recommend updating such benchmarking based on the latest market data.

In the case of fixed-rate contracts, where the benchmarking analysis has not been updated in the last three years, we also recommend that the benchmarking analysis be updated with the latest market data.

It should be noted that the fixed interest rate does not adjust to the current market situation in the same way as the interest rate under variable interest conditions based, for example, on the WIBOR rate. Consequently, we have no certainty that the comparative analysis prepared on the basis of data from a period when interest rates were much lower is still valid.

We recommend considering changing the terms of financial transactions where there is a fixed interest rate. The flexible rate adapts on an ongoing basis to market conditions in the event of changes in interest rates, which reduces the risk of the transaction terms being challenged by tax authorities. Moreover, in the case of financial transactions in the Polish zloty, by applying an interest rate based on WIBOR 3M increased by no more than the maximum margin specified in the Announcement of the Minister of Finance and meeting the requirements set forth in Article 11g of the CIT Act, it is possible to apply a safe harbour mechanism for financial transactions.

It should be remembered that a taxpayer may be exempt from the obligation to prepare a comparative analysis for a financial transaction if it meets the conditions of the safe harbour mechanism. Among other things, a certain level of interest rate is required. For financial transactions in the Polish zloty, the interest rate level may currently be a maximum of:

– WIBOR 3M + 2.8 percentage points for the borrower,

– WIBOR 3M + 2.0 percentage points for the lender.

In the case of contracts concluded at present

A taxpayer who plans to enter into a financing transaction must verify that, at the time the financing transaction is entered into, the interest rate specified in the contract

– does not exceed the maximum interest rate at the date of the loan agreement,

– against the background of the overall terms of the loan is market-based, i.e. analogous terms of the transaction would be concluded by unrelated parties.

We recommend the use of a variable interest rate when setting the terms of a financing transaction. In the case of financing in the Polish zloty (PLN), we recommend applying WIBOR + margin. Such an interest rate flexibly adapts to changes in the market of financing transactions and reduces the risk of questioning the terms of the transaction in potential tax inspections.

By applying the conditions specified in Article 11g of the CIT Act, including the flexible WIBOR 3M rate + maximum margin, as mentioned above, the transaction may enter the financial safe harbour mechanism and the taxpayer for this transaction will completely minimise the risk of questioning the conditions by tax authorities.

Note: however, the financial safe harbour does not apply to every financial transaction. An additional tool to determine the market interest rate range for a financial transaction with specific terms and conditions is the preparation of a benchmarking analysis before the terms are agreed and the financial transaction takes place.

Transfer pricing policy

A taxpayer who wants to be prepared for market changes in the company’s environment may decide to prepare its in-house transfer pricing policy. This is a document that constitutes a list of practices applied by a company or an entire capital group in the area of transfer pricing. The transfer pricing policy is a procedure that will in future govern the rules in such areas of the company as:

- valuation of transactions with related parties,

- the procedure for documenting transactions – transfer pricing documentation templates,

- the rules of collecting source documents and information necessary for documenting the transactions,

- the manager responsible for transfer pricing risk management in the company,

- preparing transfer pricing documentation and other duties in this area.

The preparation of such an enterprise policy in the form of a corporate document simplifies transfer pricing risk management. It can be concluded that most companies that have the above issues regulated in a non-formalised manner have some outline of a transfer pricing policy. However, having the transfer pricing policy in a written form puts these principles in order, creates a procedure in the company that is easily understandable for the employees responsible for the transfer pricing area in the company. Furthermore, in case of significant personnel changes, it provides a guarantee that the permanent transfer pricing policy will be continued in the company.

A well-formulated transfer pricing policy answers the question of what terms and conditions are to be applied by the company when performing financial transactions. This document should include a framework of parameters such as:

- the financing interest method used – fixed or variable interest,

- acceptable margin amounts,

- amount of possible commissions,

- principles of repayment of the financing, including the amounts of capital and interest,

- permissible loan durations,

- application of the financial safe harbour mechanism.

A taxpayer with a written transfer pricing policy minimises the risk of not applying market conditions to financial transactions in an environment of changing central bank interest rates.

If you would like support in preparing a transfer pricing policy for your company, do not hesitate to contact us by e-mail.

If you would like to find out more about the transfer pricing policy and its impact on your business, please feel free to contact us.